How companies make money in the Payments Processing Value Chain

A closer look at the economics from each $1 of payment volume

In 2019, Visa and MasterCard generated combined revenues of almost $40 billion. Meanwhile, PayPal and Square collectively generated revenues of $22 billion. And companies less visible to the everyday consumer, such as First Data, Worldpay, and Global Payments, generated revenues of another $18 billion.

When I first started researching the payments industry, it was clear that credit card processors had built large, multi-billion dollar businesses. And while several names are more commonly recognized, such as Visa, MasterCard, PayPal, and Square, there are at least 10x as many names that, though less recognized, are also formidably sized businesses.

What was far less clear to me was how payments companies made money from credit card transactions. For a quick refresher on the players in the credit card processing ecosystem, please see one of my earlier posts. If you’ve got the who’s-who covered, let’s dive in.

How payments companies make money

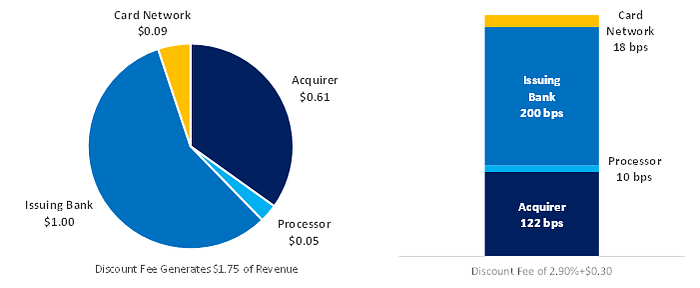

Let’s first identify the source of all payments revenues — it is called the “Discount Fee” and it is paid for by the merchant. In other words, the revenues for payments companies is an expense for the merchant.

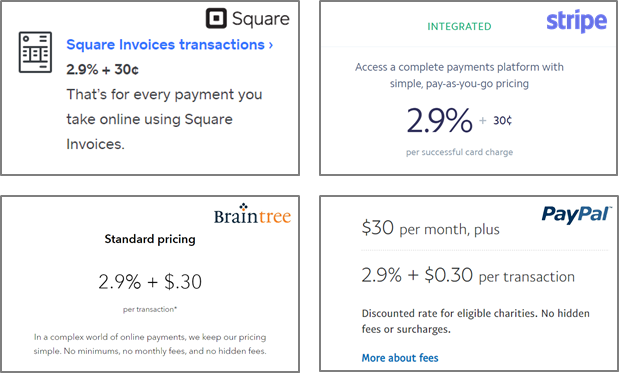

The Discount Fee is typically quoted as a percentage of the transaction dollar-amount plus a fixed cost per transaction — it looks something like 2.90%+$0.30, which means that for each transaction, the merchant pays $0.30 to the merchant acquirer, and for each $1 of transaction volume (or TPV), the merchant also pays 2.90% of that volume. As an example, here’s a screenshot from Square’s website, which lays out the possible Discount Fees for “card-not-present” transactions, i.e., when a consumer pays for a good/service without physically presenting a credit card.

From Square’s pricing page, you’ll also notice that the Discount Fee can vary greatly from one transaction to another. These variances depend largely on the perceived risk of each transaction. For example, Square charges 2.9%+$0.30 for eCommerce transactions and 3.5%+$0.15 for an in-person, but card-not-present purchase. Not shown above, but provided on another page from Square’s website is a separate menu for “card-present” transactions, which are typically considered lower risk transactions — e.g., Square’s Discount Fee for an in-person, card-present transaction is only 2.6%+$0.10.

A closer look at each of the players in the value chain

Your credit card likely has two logos on it — the bank that issued you that card (e.g., Capital One) and a card network (e.g., Visa, MasterCard). These two companies generate revenues each time you swipe your credit card. But they’re not alone! Behind the scenes, there are two other companies that take a cut each time you swipe — an Acquirer Processor and a Merchant Acquirer (a term I’ll use to collectively refer to Acquiring Banks, PayFacs, and ISOs).

- Card Networks: The industry’s “tollbooth,” the card networks collect a “network fee” on each transaction as they supply the electronic networks that enable credit card acceptance. For a standard credit card transaction, Visa and MasterCard charge a network fee of 0.14%+$0.0195.

- Issuing Banks: The banks that issue consumers their credit cards (e.g., Capital One, Wells Fargo, Bank of America) receive an “interchange fee” from each transaction. Though interchange is earned by the Issuing Banks, the interchange rates are set by the Card Networks. The full menus of possible interchange rates are published by Visa and MasterCard. These rates are also quoted as a % of TPV plus a fixed $ charge, but the interchange fee will generally range between 150 bps and 200 bps, and depends on a combination of factors, such as card type, card-present/-not-present, and merchant type, which collectively characterize the risk profile of the individual transaction.

- Acquirer Processors: Responsible for authorization, and clearing and settlement of each transaction, Acquirer Processors serve a technical role to facilitate the acceptance of each credit card transaction. In most situations, the processing service is tied to the Merchant Acquirer, so it’s difficult to parse out the stand-alone cost of the processing service. Based on a few articles I found (such as this one from Barron’s), my best guess is that the stand-alone processing fee is between $0.05 and $0.10 per transaction, and likely lower for large merchants that can drive greater volumes. If you make the rough assumption that the average transaction is $50, then the processor fee is somewhere around 10 bps.

- Merchant Acquirer: If you browse through the websites of PayPal, Stripe, Square, or First Data, you will notice that they quote the entire Discount Fee. So, it’s natural to assume that Square earns the entire Discount Fee on each transaction. However, Square does not keep all of this — remember, this is simply what the merchant pays. In fact, Square shares a large portion of the Discount Fee with the Processors, Issuing Banks, and Card Networks. The portion of the Discount Fee that the Merchant Acquirers keep, net of the amounts paid to those other parties, is termed the “Acquirer Mark-Up.”

How large is the Acquirer Mark-Up?

Square’s latest annual report reveals that in 2019 the company generated $3.1 billion of transaction-related revenues on $106 billion of TPV — this equates to an average of 290 bps. However, as I mentioned earlier, Square does not keep all of this. And as Square’s annual report reveals, in 2019 the company paid out $1.9 billion of transaction-related expenses to “third-party payments processors and financial institutions” for interchange and assessment fees, and processing fees and bank settlement fees— this implies an average of 182 bps for the sum of the expenses we discussed above, including the interchange fee (~157 bps), the network fee (~15 bps), and the processor fee (~10 bps). So for Square, its average Acquirer Mark-Up in 2019 was roughly 108 bps. My survey of some of the leading public company acquirers shows that the Acquirer Mark-Up generally ranges between 100 bps and 130 bps.

Thinking about the bigger picture

If I take a step back, and piece the various parts of the value chain back together, it’s interesting to compare the relative magnitude of the take-rates (i.e., the fee as a % of TPV) earned by each segment of the value chain, which I’ve illustrated below.

What do the take-rates reveal about competition?

What’s always been interesting to me about the payments value chain is that the take-rates within each segment are very transparent and there is little variation between competitors. And yet, there are so many start-ups and high-growth companies in payments, which I wouldn’t have expected from an industry where pricing is so stagnant and undifferentiated.

- The card networks publish their fees and there is little-to-no variability between the networks (Merchant Maverick summarizes the four major US card networks’ fees here).

- The card networks also publish the interchange fees for their issuing banks. Not only is there little variability between the rates published by Visa vs. MasterCard, but the issuing banks can’t even compete on price because the interchange rates are literally dictated to them.

- For acquirer processors, the stand-alone processing service is undifferentiated and interchangeable, so it’s safe to assume there is little pricing power.

- The merchant acquirers offer remarkably consistent pricing. It is remarkable because the acquirers can set their own pricing and they effectively take whatever is left of the Discount Fee after the other mouths have been fed. You might expect acquirers to try to compete on price. And yet, a quick look through the websites of Square, Stripe, PayPal, and Braintree, and you find this:

A closer look at the payments companies that have entered the market and successfully gained momentum in recent years — public companies like Square, Adyen, StoneCo, Lightspeed POS — and you will notice that these are all merchant acquirers. Even the private company upstarts are merchant acquirers, such as Stripe, Toast, and Checkout.com (which just announced a huge bump in its valuation earlier this week).

My only explanation for this is that the acquirers have chosen to differentiate by innovating around the quality of their service. From the emergence of the PayFac model (which I discussed in an earlier post) to the cross-selling of software and payments in the Integrated Payments model (which I plan to discuss in a future post), acquirers have enhanced their service to merchants, all while keeping their prices uniform and consistent.

Conclusion: Revenues growth for these up-and-coming payments companies depends not so much on resizing the revenue pool or taking a greater share of the revenue pool, but rather on enhancing the value proposition delivered to merchants — which can be observed with metrics such as customer growth, customer retention, and TPV growth.

Thanks for reading. Please share or follow me for my next post.

Disclaimer: The views expressed here do not necessarily reflect those of my employer.